As a BCBA, you know that parent engagement is crucial for successful ABA therapy outcomes....

As a provider of Applied Behavior Analysis (ABA) therapy, you know firsthand the importance of...

Are you a Board Certified Behavior Analyst (BCBA) or Applied Behavior Analysis (ABA) Practice Owner...

The rise of telehealth technology has opened up a world of possibilities for therapy practices....

As therapists, we are well aware that change can be difficult for our clients and...

One of the most important aspects of having a business is protecting yourself and the...

If you have any questions regarding your business or individual state requirements, don’t hesitate to...

Rethink billing software and services can help save your ABA therapy practice, clinic or...

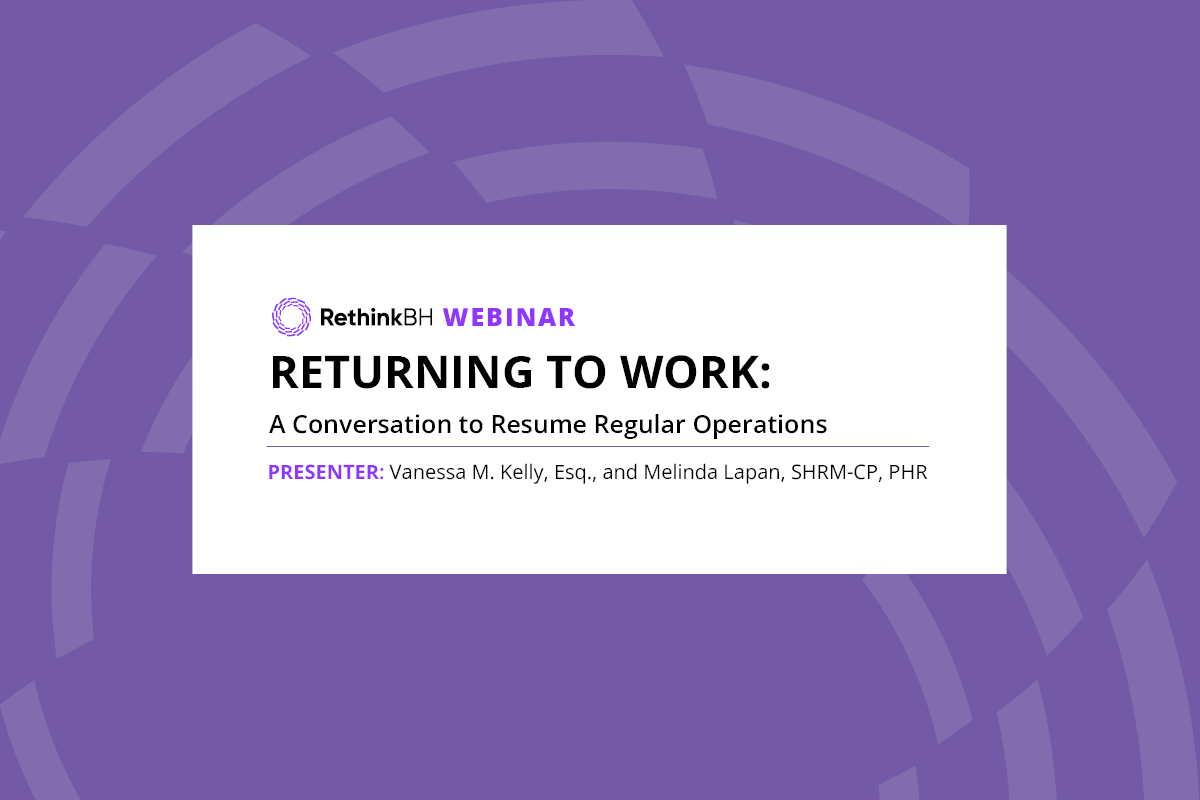

Returning to work will bring new legal and practical challenges for employers in all industries...

Introduction & Our Goal No one was expecting the COVID-19 to force practitioners to provide...

ABA therapy billing services are now available to all Rethink Behavioral Health customers! Prior to...

This piece is based on our recent webinar presented by Daniel Law, ARM, CRIS and...

Anthony Porcelli, Manager of Billing Services for RethinkBH, had the pleasure of attending Dr. Wayne...

This piece is based on our recent webinar presented by Sarah Schmitz, the Owner and...

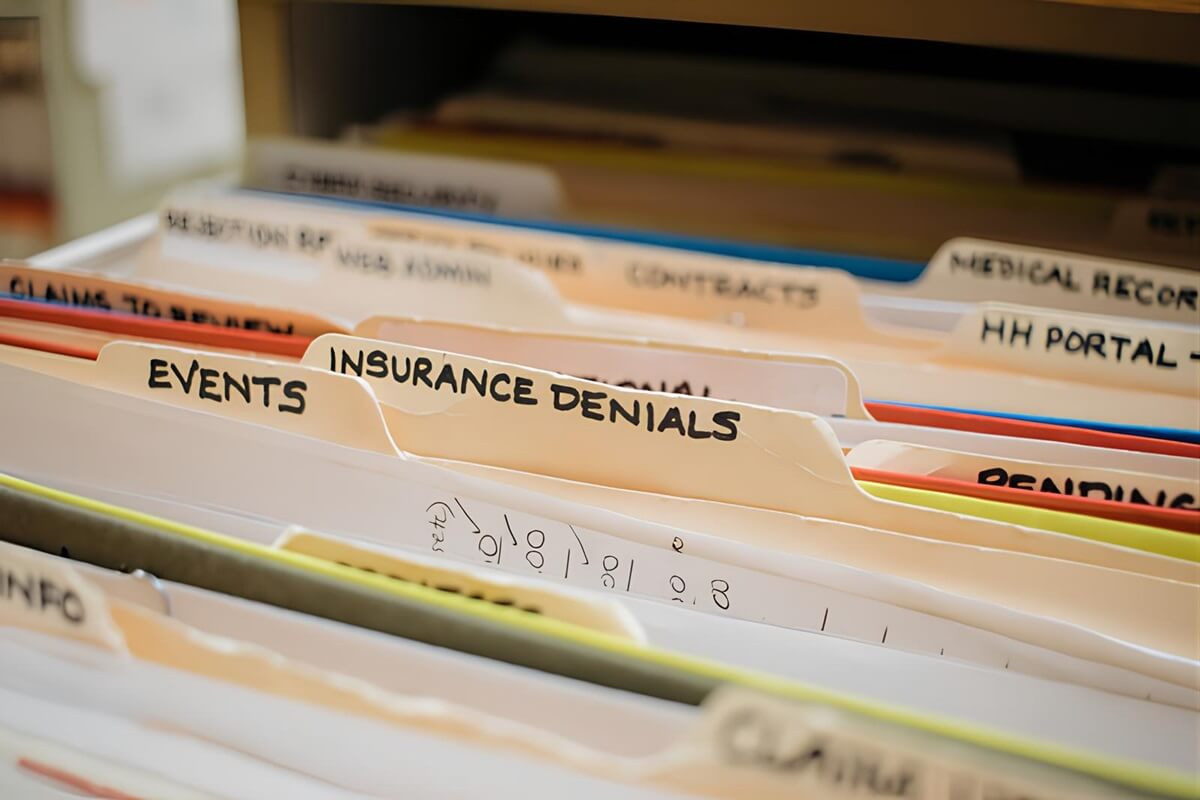

This piece is based on our recent webinar, Navigating Insurance: Unlocking the Denials & Appeals...

Over the past 14 years, Dan has focused on the design and implementation of insurance...

RethinkBH invites you to participate in our upcoming webinar, Affordable Care Act: How It Affects...

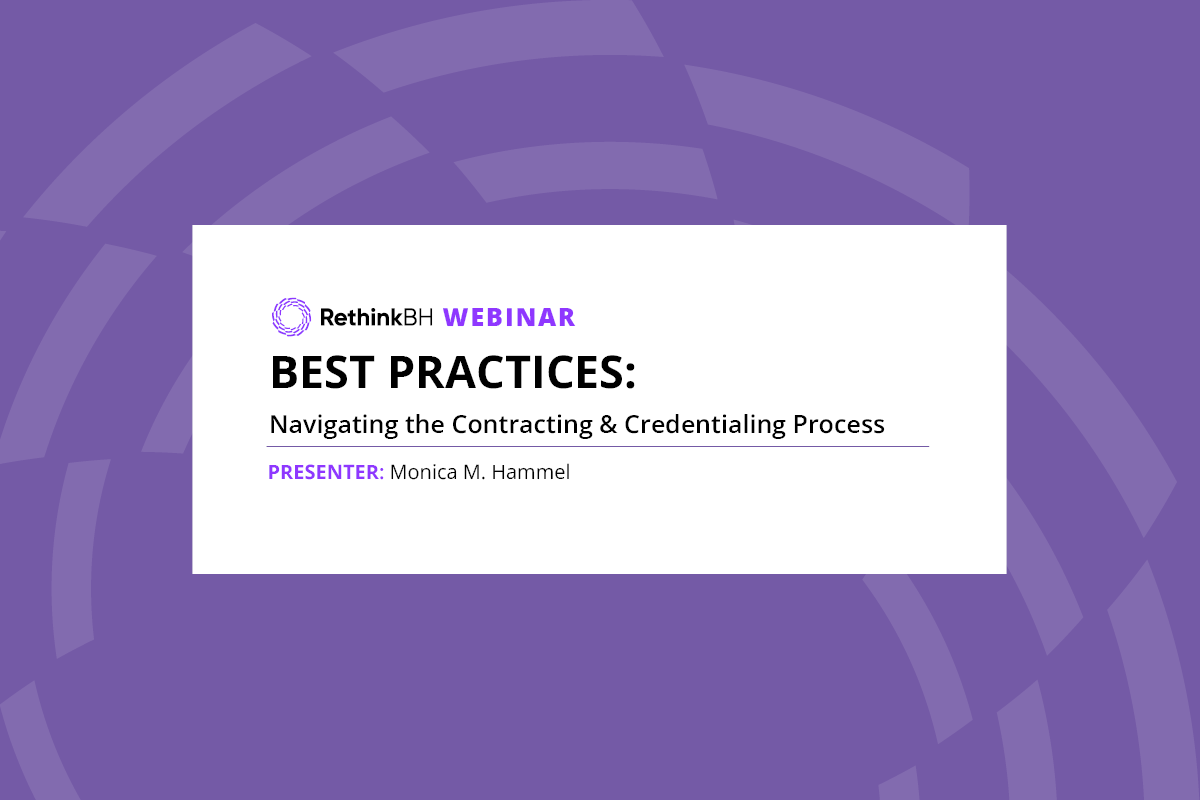

Check out our latest installment published on bSci21.org, Best Practices in Insurance Contracting! The decision...

Rethink Behavioral Health (RethinkBH) invites you to participate in our upcoming webinar, Advanced Commercial Insurance...